Why Tenant Management Impacts Property Value

Tenant management plays a pivotal role in determining both rental income and long-term capital appreciation. While many property owners focus…

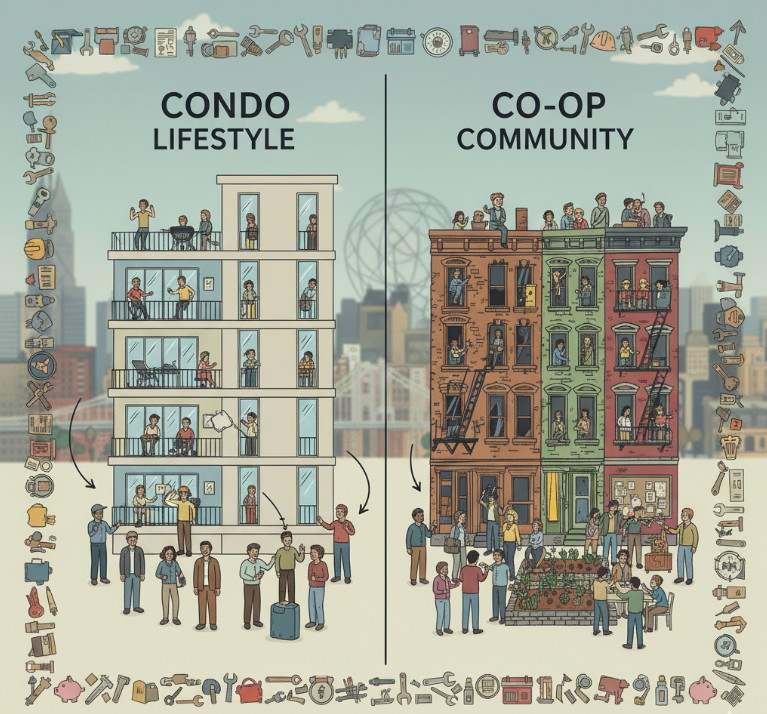

Choosing between a condo and a co-op in Queens involves understanding key differences in ownership structures, financial obligations, and lifestyle aspects. This guide breaks down everything buyers and boards need to know to make an informed decision in the ‘condo vs co-op in Queens what buyers and boards should know’ debate.

In Queens, the landscape of residential buildings is dominated by two primary types of ownership: condos and co-ops. Condominium units, or condos, are properties where buyers obtain individual ownership of specific units along with shared ownership of common areas, backed by individual deeds.

In contrast, co-ops operate under a cooperative living model where shareholders own shares in a corporation that owns the entire building, and residents receive a proprietary lease granting the right to occupy specific units. Understanding these foundational differences sets the stage for a deeper dive into the specificities of each ownership structure, especially in the discussion of co op vs other models.

Condo owners enjoy a clear-cut condominium ownership model with individual deeds that grant full ownership of their units. This deed not only signifies ownership of the specific unit but also a shared interest in the building’s common areas, including a form of partial ownership in those spaces. This dual ownership aspect means that condo owners are responsible for common charges that cover shared expenses such as maintenance of common areas, amenities, and building services.

Unlike co-op shareholders, a condo owner is solely responsible for their own property taxes, which cover property taxes not included in the common charges. This can simplify financial planning for those who prefer direct control over their tax obligations. Additionally, condo owners must insure their units and personal belongings, while the building itself is covered under a master insurance policy managed by the condo association.

This ownership structure provides a level of autonomy and flexibility that is appealing to many prospective buyers, especially those looking for a primary residence without the extensive oversight typical in co-op buildings. The condo model also tends to attract international buyers and investors due to its straightforward nature and fewer restrictions on ownership and subletting.

Co-op buildings operate under a unique ownership structure where:

The financial responsibilities for co-op shareholders are consolidated into monthly maintenance fees, which cover building expenses and address building expenses, property taxes, and sometimes mortgage and maintenance charges. This can lead to higher monthly fees compared to condos, but it simplifies the financial obligations by bundling several costs into a single payment.

Co-ops are often found in older, historic buildings and established neighborhoods, providing a sense of stability and community that’s appealing to many buyers. However, the co-op model also comes with stricter rules and regulations, as co-op boards play an active role in building operations and resident affairs, requiring a level of cooperation and community focus that differs significantly from the condo experience.

Financial considerations are paramount when deciding between a condo and a co-op. Prospective buyers must navigate differences in:

Understanding these financial aspects can help buyers make informed decisions that align with their budget and financial goals.

Generally, condos are more expensive than co-ops, with purchase prices reflecting this difference. Key points include:

However, co-ops often require higher down payments, typically ranging from 20% to 30% of the purchase price, and sometimes even higher. This can be a significant financial hurdle for some buyers, particularly those without substantial savings. In contrast, condos generally require down payments of 10% to 20%, which can make them more accessible despite their higher purchase price.

The balance between lower purchase prices and higher down payment requirements often makes co-ops an attractive option for buyers who can meet the financial requirements upfront. Conversely, condos, with their higher purchase prices but lower down payments, may appeal to those who prefer to spread their investment over time through a mortgage.

Monthly maintenance fees for co-ops are usually higher than the common charges for condos. This is primarily because co-op fees often include property taxes and the building’s underlying mortgage. These fees cover the cost of building operations, maintenance, and amenities, providing a comprehensive financial package for shareholders. The monthly maintenance fee is an important consideration for potential buyers.

In condos, monthly common charges are typically lower since they do not include property taxes, which condo owners pay separately. However, these condo fees can still be substantial, depending on the level of amenities and services provided by the condo association.

Understanding these ongoing costs is crucial for prospective buyers to ensure they can comfortably manage their monthly financial obligations.

Closing costs are an important financial consideration in any real estate transaction. For condos, these costs tend to be higher closing costs due to additional fees such as title insurance and mortgage taxes. Buyers should be prepared for these expenses, which can add a significant amount to the overall cost of purchasing a condo.

In contrast, co-op closing costs are generally lower because they do not include certain fees that are applicable to condos. This can make co-ops more appealing from a cost perspective, especially for buyers who are sensitive to upfront expenses. However, the trade-off often comes with higher monthly maintenance fees, which need to be factored into the long-term financial planning.

The approval process is another critical difference between condos and co-ops. Condos generally have a more straightforward approval process, while co-ops require a more rigorous and detailed procedure.

Understanding these processes can help a prospective buyer prepare for what lies ahead and ensure a smoother buying experience.

Buying a condo typically involves a simpler application process with minimal documentation compared to co-ops. The required paperwork usually includes standard financial documentation, building application forms, and basic background information. This streamlined process can make condos an attractive option for buyers looking for a quicker and less cumbersome approval process.

Condo boards also have the right of first refusal, meaning they can object to a sale if they choose to. However, this is relatively rare and generally does not significantly delay the buying process. As a result, condo approvals typically move more quickly than co-op approvals, providing buyers with a more efficient path to homeownership.

The co-op board approval process is known for being more rigorous and detailed compared to condos. Prospective co-op buyers must submit a comprehensive application that includes extensive financial documentation, such as tax returns, bank statements, and employment verification. This thorough financial review ensures that buyers are financially stable and capable of meeting their ongoing financial obligations as shareholders.

In addition to the financial review, co-op boards often require personal interviews and references to assess the suitability of prospective buyers for cooperative living. This can be a daunting process, as co-op boards have the authority to reject applicants without providing specific reasons. Understanding and preparing for this rigorous approval process, including the board interview, is essential for co-op buyers.

Subletting policies vary significantly between condos and co-ops, impacting the flexibility and investment potential of each. Condos generally offer more lenient subletting rules, while co-ops impose stricter regulations.

These differences can significantly affect buyer decisions, especially for those considering rental income opportunities.

Condo owners typically enjoy fewer restrictions on subletting compared to co-op owners. While there may still be some rules imposed by the condo association, these are generally less stringent than those in co-ops. This flexibility allows condo owners to generate rental income from their units when they are not in residence, making condos an attractive option for investors and those seeking additional income streams.

The more lenient subletting policies in condos enhance their long-term investment prospects by attracting a wider range of buyers, including those looking for properties with rental potential. This flexibility is one of the key reasons why condos tend to appeal more to investors compared to co-ops.

In contrast, co-ops have stricter subletting policies that can create hurdles for potential investors. Co-op shareholders typically need board approval to sublet their apartments, and this approval process can be as detailed as the purchase application process. Additionally, subletting in co-ops is often limited to a specific duration, such as one to two years out of every five years.

Subletting in co-ops requires shareholders to submit an application, undergo a background check, and receive board approval, often making it a time-consuming and uncertain process. These stringent rules can deter investors and those looking for flexible rental options, making co-ops less attractive for short-term investment purposes.

The governance and responsibilities of condo and co-op boards play a crucial role in the management and operation of the buildings.

Understanding these differences can help prospective buyers and current residents navigate their living environments more effectively.

Condo boards are responsible for managing the operations and common areas of the building, ensuring compliance with building rules, and maintaining the property. They can also impose fines and seek court injunctions for rule infractions, but they typically take a more hands-off approach compared to co-op boards.

The condo board’s responsibilities include working with a management company to handle day-to-day operations and ensuring that the building runs smoothly. This professional management approach often results in efficient operations and a well-maintained property, enhancing the living experience for condo owners.

Co-op boards, on the other hand, have more direct authority over building operations and resident affairs. They are responsible for approving new shareholders, reviewing financial qualifications, and addressing individual shareholder issues. This hands-on approach means that co-op boards play a more active role in the daily management of the building.

In addition to managing building operations, co-op boards have the authority to make decisions regarding evictions, a power not held by condo boards. This level of control allows co-op boards to maintain a stable and cohesive community, but it also comes with a higher level of oversight and involvement in residents’ lives.

The differences in lifestyle and community between condos and co-ops can significantly affect buyer decisions. Condos offer flexibility and modern amenities, while co-ops provide stability and a strong sense of community. When considering a purchase, it’s essential to weigh the pros and cons of co op vs condo.

Personal preference plays a crucial role in determining which option is best suited for an individual’s needs and lifestyle.

Condos often attract buyers with their contemporary architecture and design, reflecting modern living preferences. Many condos are situated in newly constructed condo buildings that offer a range of modern amenities, such as:

These amenities enhance the overall living experience, providing convenience and luxury to residents.

The flexibility of condo ownership also appeals to those seeking a dynamic lifestyle. The lenient subletting policies, combined with the modern amenities, make NYC condos an attractive option for young professionals, international investors, and those looking for a primary residence with the potential for rental income. This flexibility, coupled with the appeal of modern living spaces, makes condos a popular choice in the competitive NYC real estate market.

Co-ops are designed with a focus on stability and long-term residency, making them ideal for buyers who value a strong sense of community and permanence. Residents in co-ops often develop closer relationships with their neighbors, fostering a sense of camaraderie and mutual support. This community-oriented living environment can be particularly appealing to families and individuals seeking a stable and supportive neighborhood, such as those looking for a co op apartment.

The stability of co-op living allows residents to invest in their living environment for years to come, contributing to the overall well-being and maintenance of the building. However, this stability comes with stricter regulations and a higher level of involvement from the co-op board, which can impact personal freedoms and flexibility.

Despite these trade-offs, many buyers find the community focus and long-term stability of co-ops to be a compelling choice.

Investment potential and resale value are critical factors for prospective buyers considering condos and co-ops. Condos are generally viewed as more appealing investments due to their higher market liquidity and fewer restrictions, while co-ops offer less flexibility but can still provide a stable investment for long-term residents.

Condos typically have a higher resale value than co-ops, making them a more attractive option for investors. On average, condos resell for 25-30% more per square foot compared to co-ops, reflecting their favorable ownership structure and market appeal. This higher resale value is due to the broader range of buyers condos attract, including international investors and those seeking rental income opportunities.

In contrast, co-ops often have resale prices about 25-30% lower per square foot than condos. The more stringent approval processes and subletting restrictions can limit the pool of potential buyers, making co-ops harder to sell. Additionally, co-ops outnumber condos in many markets.

However, for buyers looking for long-term residence and community involvement, the lower resale value may be a secondary consideration to the benefits of cooperative living.

The long-term financial benefits of owning condos often include a stable appreciation rate, driven by continuous demand from diverse buyer demographics. Condos tend to maintain a higher median price due to simpler transaction processes and strong demand, making them a reliable long-term investment. This stability in value is particularly appealing to international investors and those looking for a secure investment in NYC real estate.

Conversely, co-ops can offer long-term stability but may not appreciate as quickly as condos. The cooperative ownership model, while beneficial for community living, can limit the market appeal and resale value.

However, for buyers focused on long-term residency and community engagement, co-ops can still provide a valuable and stable investment over time.

Legal and regulatory considerations are essential for both buyers and boards to ensure compliance and protect interests. Understanding these aspects can help navigate the complexities of condo and co-op transactions and ensure a smooth and legally sound buying experience.

Prospective buyers must receive detailed disclosures about the physical condition of the property in offering plans to ensure informed decision-making. Legal protections such as the Housing Merchant Limited Warranty Law guarantee one year of protection against defects for newly constructed homes, enhancing buyer security. These protections are crucial in ensuring transparency and fairness in the buying process, providing buyers with the information they need to make informed decisions.

Both condos and co-ops provide legal protections that contribute to informed buying decisions. By understanding their rights and the condition of the property, buyers can navigate the buying process with confidence and security, ensuring their interests are protected throughout the transaction.

Regulatory compliance is a crucial aspect for condo and co-op boards to uphold to maintain legal and operational standards. Minutes from board meetings provide critical insights into ongoing issues and regulatory compliance, helping prospective buyers understand how the board manages the building. Transparency in board governance, reflected through documented meeting minutes, is essential for building confidence among residents and potential buyers.

Understanding how boards manage compliance can significantly affect buyer decisions and trust in the community. Boards must ensure they adhere to local laws and regulations, maintain transparency, and effectively manage building operations to foster a stable and compliant living environment.

Selecting the right property management company is vital for the efficient management of condos and co-ops. A capable property management team can enhance operational efficiency, ensure regulatory compliance, and improve tenant satisfaction.

Hiring experts in property management allows owners to focus on investments without being bogged down by day-to-day operations. Experienced property managers conduct thorough tenant screenings, minimizing the risk of renting to unreliable residents and ensuring a stable tenant base. This professional approach to management can lead to increased efficiency and peace of mind for property owners, enhancing the overall value and appeal of the property.

Professional property management companies bring expertise to managing properties effectively, handling everything from maintenance oversight to legal compliance. This comprehensive management approach ensures that the building runs smoothly and meets the needs of both owners and tenants, contributing to a positive living environment.

A good property management firm should demonstrate strong communication skills to keep owners informed and engaged. Clear and effective communication facilitates smooth interactions between owners and tenants, ensuring that issues are promptly addressed and resolved. This level of responsiveness and transparency is crucial for maintaining a well-managed property.

When selecting a property management company, it’s important to consider their experience and understanding of local market dynamics. A qualified management company can enhance the efficiency and management of your building, ensuring that it remains a desirable place to live and invest.

For tailored property management services in New York City, contact Vanderbilt NYC APT. We specialize in providing comprehensive solutions designed to protect your investment and simplify day-to-day operations.

Our services include:

At Vanderbilt NYC APT, we emphasize strong communication with both property owners and tenants. By maintaining open, transparent dialogue, we streamline the process of handling requests, addressing concerns, and ensuring smooth operations across every property we manage.

We also provide free consultations to help you explore customized management strategies that fit your needs. Whether you own a single unit or multiple buildings, you can rely on us for expertise, professionalism, and a commitment to protecting your real estate investments.

Visit us at 45-02 Ditmars Blvd, Suite 1016, Astoria, NY, or contact us today to schedule your consultation and discover how we can make property management stress-free.

Choosing between a condo and a co-op in Queens involves careful consideration of various factors, including ownership structure, financial requirements, approval processes, subletting policies, and board governance. Condos offer flexibility, modern amenities, and higher resale values, making them attractive for investors and those seeking contemporary living spaces. Co-ops, on the other hand, provide stability and a strong sense of community, appealing to buyers looking for long-term residency. Understanding these differences can help buyers make informed decisions that align with their financial goals and lifestyle preferences.

The main differences between condo and co-op ownership are that condo owners hold individual deeds and own their specific units, whereas co-op shareholders own shares in a corporation and possess a proprietary lease for their occupancy.

Condos are typically more expensive to purchase than co-ops, although co-ops may involve larger down payment requirements.

Co-op shareholders are required to pay monthly maintenance fees that encompass building expenses, property taxes, and occasionally underlying mortgages. It is essential to account for these financial obligations when considering co-op ownership.

Co-ops enforce stricter subletting policies that typically require board approval and may impose limits on the duration of sublets, in contrast to the more flexible rules found in condos.

When choosing a property management company, prioritize those with strong communication skills, local market expertise, and a proven track record of effective management. This ensures that your property is handled professionally and efficiently.